Once people find out I’m an investment manager, I’m often asked, “What should I be invested in?”

Here’s the answer. For an investment portfolio to do well and stand the test of time, it should have these four elements:

1. It should be diversified.

2. Its mix of stocks and bonds should be consistent with your “emotional speed limit.”

3. It has a lean expense structure (has no mutual funds with sales “loads” and uses Index Funds)

4. It has a mechanism to protect against market disasters.

Let me elaborate on each of these.

1. It should be diversified.

Known as one of the few “free lunches” of finance, diversification helps make sure that when one of your investment eggs crack, you still have many others that will survive. I like pictures, and our brains are hard wired to like them too, so here’s an illustration by Bernstein that shows how diversifying can help capture a higher average rate of return while reducing your downside risk:

Diversification helps you eliminate your downside more than it reduces your upside potential.

How many stocks do you need? At least 10-20. Once you reach 10 stocks, you have captured 83.6% of the benefits of diversification. At 20, you capture 91.8%, at 50, you capture 96.7%, and at 400, you capture 100% (source).

Yes, diversification is good. But do not fall into the trap of thinking you need that many diversified mutual funds or ETFs (which stands for Exchange Traded Fund). Mutual funds already usually have at least 100 stocks in their portfolios. You don’t really need more than about 5 funds, since you will likely already have 500 stocks. But if you’re only in concentrated sector funds, there is more room for additional funds, since having 50 internet stocks or 50 energy stocks isn’t really being diversified.

2. Its mix of stocks and bonds should be consistent with your “emotional speed limit.”

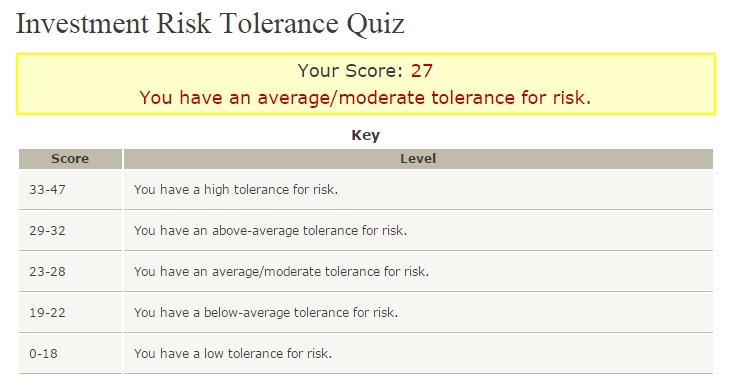

How much pain can you handle when you look at your investment statements? People don’t usually know the answer to this question until it’s too late. So to save you time, I found a really good online quiz from Rutgers University that has one of the more creative ways I’ve seen to determine what your risk tolerance is. It’s 20 questions, and it probably takes about 2 minutes to complete.

I took the quiz. Here’s what my results looked like:

Once you know what area you fall under, you can roughly translate that into how much you could have in terms of a stock/bond mix:

High tolerance: 80-100% stocks

Above Average: 60-80% stocks

Average: 40-60% stocks

Below Average: 20-40% stocks

Low tolerance: 0-20% stocks

If you’re finding out just now that your stock exposure is beyond your risk tolerance, you are going above your emotional speed limit. It increases the risk that you’ll either a) sell out of the market at the worst time or b) feel extreme discomfort when markets go into a bear market and you will hate life and everyone around you until it recovers. Tap on the brakes a little, and you’ll find you’ll be able to sleep better at night.

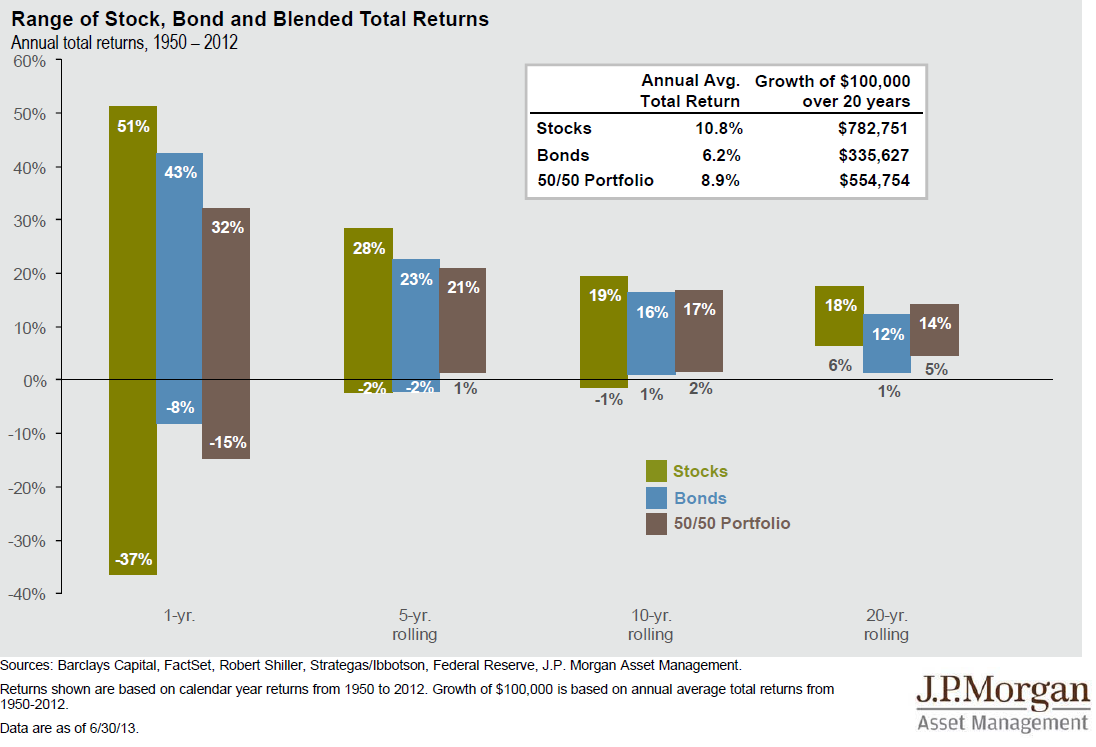

Note: It’s worth mentioning that the more years you have available to invest, the larger the percentage in stocks you can have (and if you have less time, the smaller it should be). That’s because the probability of loss goes down significantly over time. See the following infographic from JP Morgan.

|

| (Click to enlarge) |

3. It has a lean expense structure (has no mutual funds with sales “loads” and uses Index Funds)

Costs kill investment performance. It’s that simple. Which is why it’s so baffling to see many investment statements still having mutual funds that charge sales fees that go as high as 5.75%. This isn’t the 1990s anymore. Since then, costs have plummeted and there are literally thousands of mutual funds and ETFs that you can invest in that have zero sales charges. For a $10,000 purchase of a mutual fund that charges a 5.75% sales load, why would you pay a broker $575 when online brokers like Scottrade let you buy an ETF with similar return characteristics for $7?

Think of your investment portfolio like a race car. Now think of fees like extra lead weights. Which would win in a race, the one with lead weights, or the one without it? Exactly. Keep your race car light and lean, and you stand a much better chance of winning the investment race over the long term. (For more perspective, see this article “Fees matter more than asset allocation”.)

Don’t know if you’re paying a sales load for your mutual funds? Go to Morningstar.com and type in your fund symbol. Look for “Load” and “Expenses” – if there is a Load, you have lead weights in your car. And if the Expenses are larger than 0.20%, you are likely paying for performance that could be closely approximated by lower expense ETFs.

And if your broker won’t steer you into lower costing investments, it might be time to rethink who he’s looking out for, you or him.

Stock market returns are projected to be as low as 3%-5% for the next decade, so keeping your costs as low as possible will play a large role in your returns.

4. It has a mechanism to protect against market disasters.

Markets go up about 70% of the time. For the other 30%, it can cause a lot of heartache like when stocks fell as much as 50% in 2000-2002 and 2008. Research suggests that investors move like herds, and over a 12 month period, when markets go up, the likelihood of it moving up again the next year is high, and when markets go down over a 12 month period, the likelihood of it going down again the next year is also high, because of this herd/momentum effect.

It means that there is a critical Tipping Point when that positive momentum turns into negative momentum…

…and if you use that rolling 12-month signal when stocks turn negative to become more defensive with your portfolio and shift your allocation to investment grade bonds, you tend to do pretty well historically. Over the past 20 years, using this approach, you would have been able to avoid the 2008 financial crisis, and you would have been able to get out shortly after the peak of the dot-com bubble.

What we find is that by playing good defense, your offensive numbers tend to improve. That is our basic approach. We are not trying to hit home runs. Rather, we are trying to just avoid those big disasters, and when you do that, you tend to do pretty well.

And that’s it. If you have the above four ingredients to guide your investment portfolio, you stand a very good chance of doing well over time. And if you don’t, I invite you to book a time on our calendar to get your portfolio on the right footing for the upcoming year.

—————————— About Parabolic Asset Management ——————————-

• Experienced: Over 15 years of experience, spanning three bull markets and two bear markets. Managed $100 million at Wells Fargo’s Wealth Management division and co-managed a $50 million hedge fund.

• Experienced: Over 15 years of experience, spanning three bull markets and two bear markets. Managed $100 million at Wells Fargo’s Wealth Management division and co-managed a $50 million hedge fund.

• No Conflicts Of Interest: You get unbiased advice because we don’t sell commissioned products. Fee is 1% of AUM (learn more).

• Your Interests Come First: We are held to the Fiduciary Standard, not the Suitability Standard.

• Avoid High Expenses: Index funds have up to 90% lower fees than actively-managed mutual funds and outperform them over the long term. Don’t own them? You may be paying too much.

• Held to the CFA Code of Ethics: Our firm believes in operating with integrity and abiding by the highest ethical and professional standards in the industry.

Rainier Trinidad, CFA

San Diego and Coronado’s Fiduciary Financial Advisor

Parabolic Asset Management

rainier@parabolic.us

(619) 888-4070

Investment Risk Disclaimers: (i) Investments involve risk and are not guaranteed to appreciate, and (ii) Past performance is no guarantee of future results.