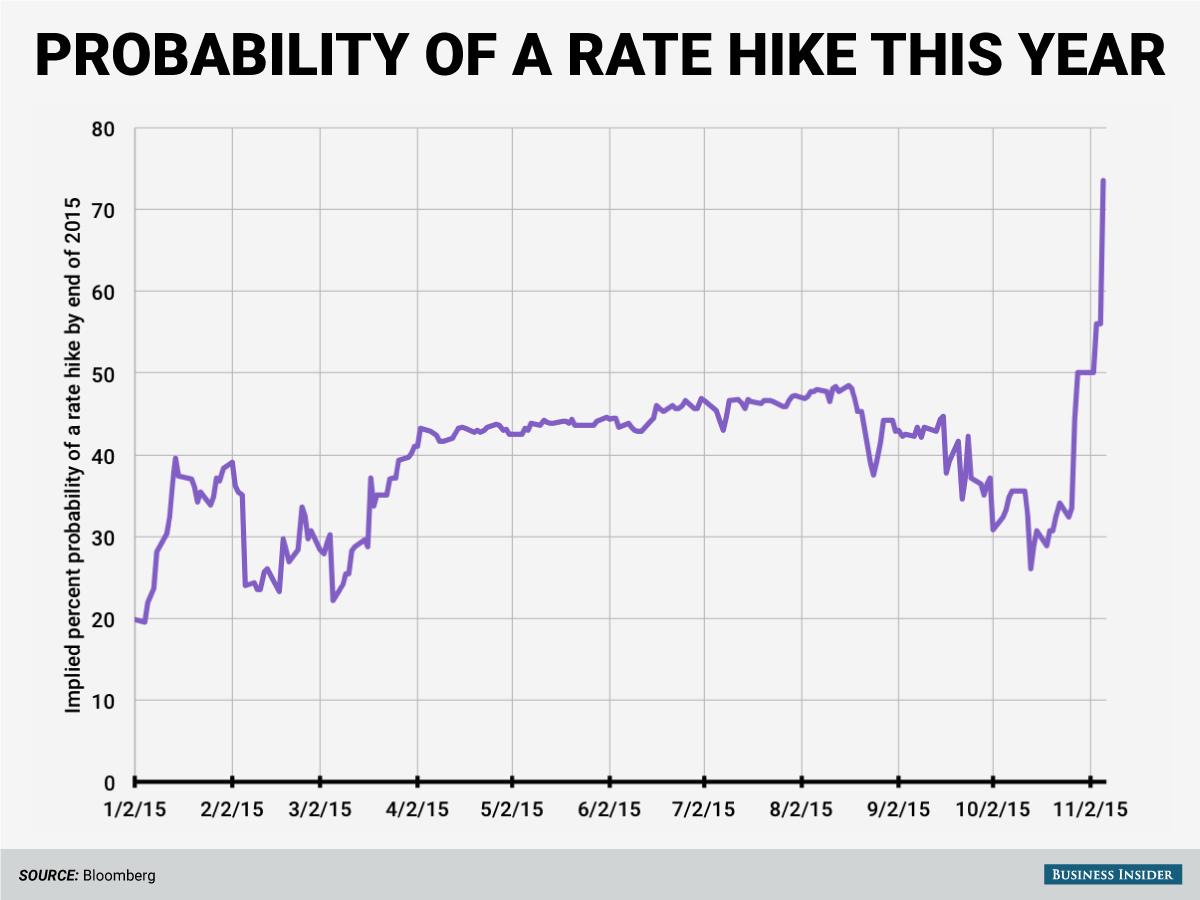

Last week’s stronger-than-expected jobs report blew apart the expectation that the Federal Reserve would stay on the sidelines until next year to raise interest rates. Here’s a graph of the market’s expectations:

So now what? Does that mean you should dump your bonds? A lot of people have been playing it safe for the past few years, keeping their “duration” short by owning only short term bonds that get hurt less when interest rates rise. Rick Ferri had a great article on Forbes that illustrated the tremendous opportunity cost of staying on the short end of the duration spectrum for the past few years in order to avoid the rise in interest rates (for those who didn’t read the article, it basically said: don’t do it).

Here’s the thinking behind why someone might do that. First, we need to understand the visual relationship between interest rates and bond prices. Think of it like a lever: the farther out you are on the lever, the more it moves. So bonds that mature in 2-3 years will move less than bonds that mature in 20-30 years.

|

| The relationship between interest rates and bond prices (source) |

So from this perspective, because bond prices will move down when interest rates move up, a lot of people huddled on the short end to avoid larger price declines. What is often forgotten is that when interest rates go up, the income component will also rise, which will offset part of the price decline. Over the past 40 years, about 93% of a bond portfolio’s returns have come from the income component, not the price movement (source).

Now let’s look at the historical evidence for what has happened in the past three times interest rates went up (source: Nuveen):

|

| Bonds have done fairly well in recent rising interest rate environments. Click for a larger view (source) |

As you can see, in all three periods, the Broad Bond Market fared all right and delivered positive returns (though the ’94/’95 period was a squeaker). Even though narrower segments within the bond market fared poorly, other areas made up for it with positive returns.

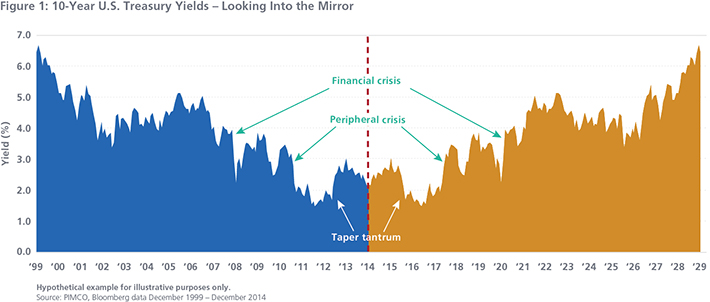

And for another great perspective, take a look at PIMCO’s work on what would happen to bonds if interest rates went back up at the same rate that they fell over the past 15 years. Yields would hypothetically look like this:

One would tend to think that returns would be disastrous for bonds, because as yields rise, the prices of bonds fall. The article goes on to explain that while the prices do indeed fall, the higher interest income actually more than offsets the lower prices. The results are astounding: if, hypothetically, 10-year Treasury yields went back up to 6.44% by the end of 2029 (up from 2.17% at the end of December 2014), their simulated 15 year rate of return is a positive 2.00% – 2.50% per year going forward, depending on the “duration” of the bond:

And don’t forget: bonds are an essential component of a portfolio in terms of diversification. In my post during the recent market correction (“Why Diversification Won and Lost Today“), I highlighted the benefits of having bonds in your portfolio. They often zig when the market zags and they tend to hold up well during periods of panic.

So to conclude, don’t get rid of those bonds. Stay broadly diversified by holding a nice aggregate bond index, and be patient.

(Posted November 11, 2015)

• Experienced: Over 15 years of experience, spanning three bull markets and two bear markets. Managed $100 million at Wells Fargo’s Wealth Management division and co-managed a $50 million hedge fund.

• Experienced: Over 15 years of experience, spanning three bull markets and two bear markets. Managed $100 million at Wells Fargo’s Wealth Management division and co-managed a $50 million hedge fund.

• No Conflicts Of Interest: You get unbiased advice because we don’t sell commissioned products. Fee is 1% of AUM (learn more).

• Your Interests Come First: We are held to the Fiduciary Standard, not the Suitability Standard.

• Avoid High Expenses: Index funds have up to 90% lower fees than actively-managed mutual funds and outperform them over the long term. Don’t own them? You may be paying too much.

• Held to the CFA Code of Ethics: Our firm believes in operating with integrity and abiding by the highest ethical and professional standards in the industry.

Rainier Trinidad, CFA

San Diego and Coronado’s Fiduciary Financial Advisor

Parabolic Asset Management

206 J Avenue

Coronado, CA 92118

rainier@parabolic.us

(619) 888-4070

Investment Risk Disclaimers: (i) Investments involve risk and are not guaranteed to appreciate, and (ii) Past performance is no guarantee of future results.