(Posted July 11, 2016)

We live in interesting times.

When trying to make sense of the direction and level of the stock and bond market, there is one narrative that seems to fit best, and that revolves around the following central ideas:

1) The economy’s growth is highly dependent on the perception that we all feel wealthy. The more wealthy we feel, the more we are willing to spend. This is called the Wealth Effect.

It is because of this central tenet that the Federal Reserve has done all it can to keep asset values high in the stock market. High values make people feel wealthy, and therefore, spend more. When the 2008 Financial Crisis happened, the Fed drove interest rates down to zero to spur economic activity, hoping that it would increase borrowing and investment by companies to spur economic growth. But by doing that, it also had the following consequence: savers who depended on the 5% yields from guaranteed CDs were now faced with puny returns of sub-1% returns.

Where were these savers going to go? Well, it forced them to go further out on the risk spectrum and buy stocks that were yielding 2-4%. The lower interest rates drove people out of the CD market and into the stock market, and now we’re sitting near all time highs. From the Fed’s standpoint, it was Mission Accomplished, and people continued to spend as their increased wealth from the stock market gave them confidence.

2) The Wealth Effect and low interest rates aren’t leading to much growth in the economy.

But the other half of the equation, the spending by companies to spur economic growth, didn’t happen, and it’s caused some problems. What we’ve seen instead is that the lower the interest rates went, the slower the economy grew.

Why?

Think of it like this: imagine you are a business owner, and you have a partner that owns a good chunk of the business. If you ever wanted to buy him out, it used to cost maybe 7% to take out a loan to buy out that interest, but with interest rates being significantly lower now, you can take out a loan for only 3%, for example. It becomes a lot cheaper to buy back and own more of your business as interest rates fall.

There’s a crowding out effect taking place here: instead of borrowing money to fund future equipment and expansions, you’ve decided to use those loan proceeds to buy out a larger proportion of the business.

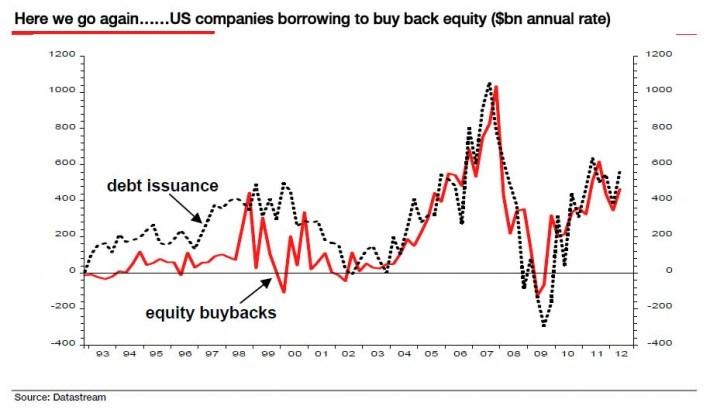

And that’s exactly what’s happened in the stock market: a large proportion of the money being raised in the debt markets isn’t being used to fund capital expenditures (known as CapEx) or research & development (known as R&D), but instead to buy back shares. Here’s a graph that illustrates the trend (source).

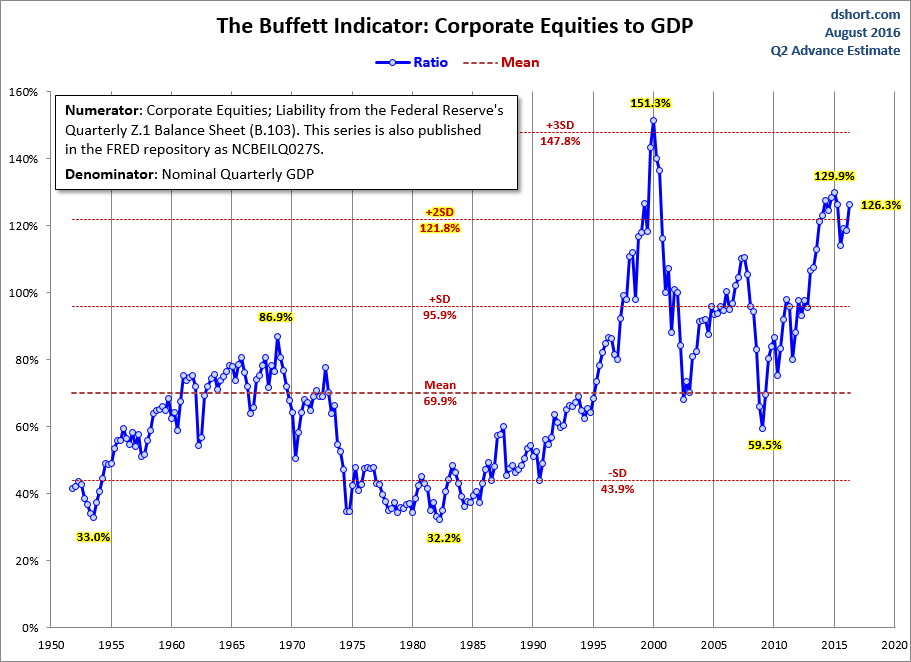

As the cost of debt went down, it became cheaper to buy back shares, and money got diverted to financial engineering (buying back shares to increase reported earnings per share) instead of future drivers of growth. And buybacks have been elevated despite the market becoming even more expensive. The combined value of all the stocks now exceeds the entire US GDP by 19% (historically the ratio of stocks to GDP was around 0.70, but is now at 1.19), which is the second most expensive in history.

And with international economies and stock markets being weak and foreign interest rates being in negative territory, we have narrowed the available supply of healthy markets to just one: the US stock and bond market.

3) This has led to the increased perception that There Is No Alternative when it comes to where to park your investment dollars, leading to the term known as TINA.

Because of the lack of alternatives, it has also led to the increasingly dangerous belief that valuations do not matter very much, because everyone has to invest in the US market. The most important factor seems to be this: As long as the Federal Reserve is willing to keep interest rates near zero, the game can continue, since the savers have no alternative to go back to (and share buybacks can continue at cheap rates). And with the Brexit event passing, it gave market participants every reason to think that the timing of interest rate increases has been pushed back to as far as 2018, so the markets went straight up, despite the vote actually causing earnings projections to soften.

The market’s sharp upward move has created the perception that stocks can only go up, and it has pulled us into Greed territory, according to CNN’s Fear & Greed Index:

The increased risks from high valuations and soft earnings (earnings have fallen for four straight quarters, and the widening gap between real GAAP earnings vs pro forma “what we want you to see” earnings) have led to a stampede in bond buying, which drove interest rates to new lows as investors looked for some sense of safety. And gold, which is also recognized as a safe haven, has rallied strongly.

And this is also what happens with the TINA narrative: the gap between stock prices and earnings decouples. The following is a graph of the S&P 500 and GAAP earnings (source). You can see that even though earnings have fallen to 2013 levels, the market is now at all time highs. This gap between earnings and stock prices is the single most important risk to the market right now, and we are controlling for it by maintaining a more conservative asset allocation.

So the other problem is this: there are some who believe that since bond interest rates are so low, it makes stocks relatively more attractive because they yield more than bonds. This kind of circular thinking is dangerous, and fails to see the point that bond yields are low precisely because of the high perceived risk in other investment alternatives.

The China economic weakness spill-over risk earlier in January and February and Brexit in June has taught us that “it’s not our problem,” and as long as the US has an accommodating Federal Reserve, as long as savers have no other alternative to park their cash, and earnings have an upward path at the end of the tunnel, the US stock market is the place to be and that earnings and valuations don’t matter very much.

This is why we have the convoluted situation where “bad news is good news” – because bad or soft economic news means the Federal Reserve can’t raise / normalize interest rates, while strong economic figures reintroduces the risk that rates will rise and end the party. The only way forward is with the Goldilocks path: just enough growth to increase earnings, but not enough to cause inflation to move upward and cause interest rates to rise.

So the risks are as follows: if the economy gets strong enough that inflation comes back to the Fed’s target rate, rates will rise and derail the near-zero interest rate policy. The last time interest rates rose in mid December 2015, stocks fell 9% in the following month. If the economy enters a recession, bad news this time will indeed be bad news because there isn’t much room left from the monetary policy side to help the economy anymore (which is why the Fed wants to raise rates so they have ammo the next time the economy heads south). If rates are near zero, you don’t have much more room to do anything else, except maybe go to negative interest rates, and that would destroy banks and have other unintended consequences.

Despite the above cautionary points, as long as jobs growth remains positive, which is the case so far, there is still some room for the market to go higher (source).

In addition, earnings estimates are calling for a significant jump of 13.4% in 2017 vs 2016 (source):

Each dollar of earnings the market is willing to pay for is now costing much more, however, with the trailing P/E now at 24.7x (source), so any disappointment to those projections will have a proportionately higher impact to the downside for stocks.

Overall, the market is walking a very fine line, and gold prices and bond prices are betting it can’t for much longer. Can it walk the line? We don’t know, but there is a small light at the end of the tunnel if we can meet the growth expectations of 2017.

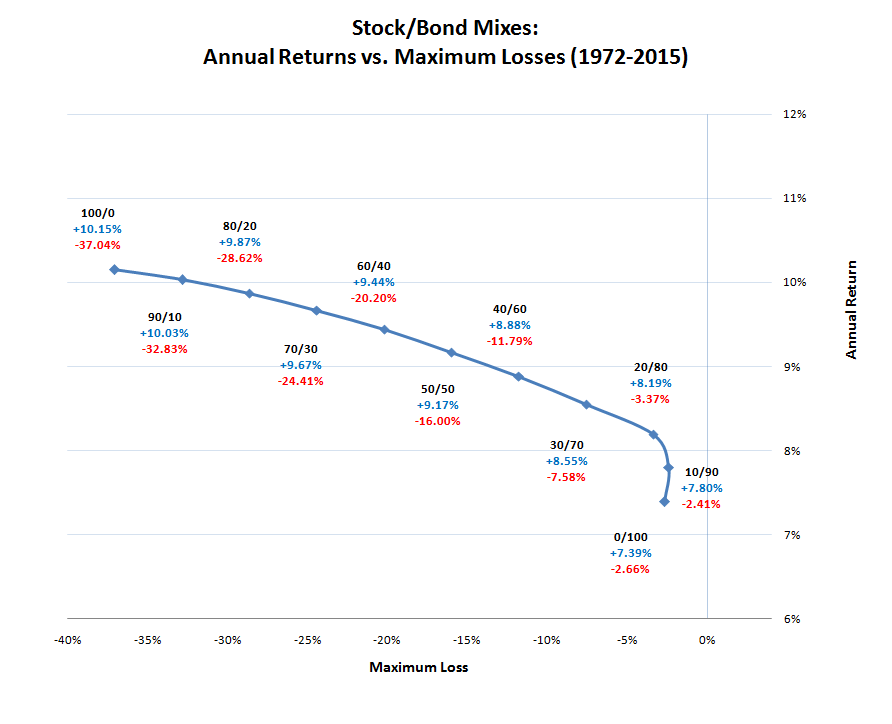

With stocks at all time highs and bond yields near all time lows because of high perceived risk, I’ve never seen this kind of configuration in the markets before, so this time, it may indeed be different, but the historian in me always fears the outcome whenever it has been perceived to be different and valuations haven’t mattered. It’s when valuations matter least that it matters most to have some method of protecting your investment portfolios from loss, which is why we remain invested, but with more conservative asset allocations. We are happy to give up a little return in order to gain a lot from reduced downside, as this graph below shows:

|

| Give Up A Little Return, Gain A Lot From Reduced Downside |

We have succeeded in the past by playing good defense, and we will continue to implement this policy in this current environment for clients.

Rainier Trinidad, CFA

San Diego and Coronado’s Fiduciary Financial Advisor

Parabolic Asset Management

206 J Avenue

Coronado, CA 92118

rainier@parabolic.us

(619) 888-4070

Investment Risk Disclaimers: (i) Investments involve risk and are not guaranteed to appreciate, and (ii) Past performance is no guarantee of future results.