(Posted June 11, 2016)

It is often said that the markets climb a wall of worry. Here is the current wall I am climbing:

1. Earnings quality has deteriorated.

The earnings that companies like to present to Wall Street often have a layer of lipstick on them to make them look better than they actually are. These are called “pro forma earnings” and are defined as:

“…earnings that have been adjusted from regular GAAP (generally accepted accounting principles), usually by excluding one or more costs to give what the preparer believes is a truer picture of its underlying profitability…”

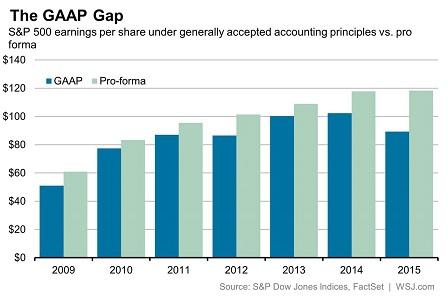

Fortunately, companies are required by the law to present the actual earnings, known as GAAP earnings, so investors have a true view of a company’s performance, unaltered by a CEO’s spin.

Here is how the gap between GAAP (real earnings) has widened from pro forma earnings (earnings that hide unpleasant and inconvenient truths) (source):

The wider the gap, the lower the quality of reported earnings. And when earnings quality deteriorates, that’s when trouble tends to happen more frequently as the sustainability of stock prices becomes more tentative.

2. The price investors are willing to pay for each dollar of earnings has risen significantly:

Here is a graph of the trailing GAAP P/E ratio over time. It shows how much the market has paid for the last 12 months of GAAP earnings (source):

Yes, of course the market is a future looking mechanism, since the market likes to believe it before it sees it, but pretty much every year since I’ve been managing investments (17 years and counting), there was always a greater hope being held that the second half of the year would have better earnings, and therefore the future P/E wouldn’t be so high.

The problem is, Wall Street analyst play this game where their annual projected earnings start out high (which justifies the argument that the forward P/E ratio will be low), but by the end of the year, the majority of the time, those earnings estimates fail to materialize and have to be revised lower. Here’s how the revision history looks (source). Notice how it tends to start out high and then falls throughout the year:

When pro forma earnings have this wide of a gap vs GAAP earnings and the amount investors are paying for a dollar of real earnings is this high, under a more traditional environment (in which the Federal Reserve doesn’t prop up the markets by punishing savers and driving them further out into the risk spectrum), it usually bodes poorly for future returns.

As I have recently stated, I continue to hold a cautious stance on the market and preach a more conservative asset allocation that strikes a good balance between stocks and bonds. Overweighting equities to reach for that extra rate of return has unfavorable prospects, in my opinion.

Rainier Trinidad, CFA

San Diego and Coronado’s Fiduciary Financial Advisor

Parabolic Asset Management

206 J Avenue

Coronado, CA 92118

rainier@parabolic.us

(619) 888-4070

Investment Risk Disclaimers: (i) Investments involve risk and are not guaranteed to appreciate, and (ii) Past performance is no guarantee of future results.