If you’re nearing retirement or recently entered it, then you’re in what’s called the “Retirement Red Zone®” – a phrase coined by Prudential that designates the five years before and five years after retirement.

It’s at this critical point that you’re subject to what is called Sequence Risk, the risk that you would experience lower or negative returns just when you start making regular withdrawals from your retirement account.

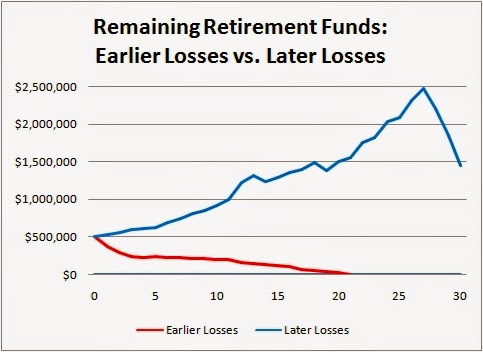

Let’s take two 30-year periods, the first having three down years, -20%, -15%, and -10%, followed by a fairly stable set of returns that causes the average annualized return to be 6.0% by the end of 30 years.

And let’s have the second 30-year period exactly reverse the above sequence of returns, where it experiences those down years at the very end, and also having average annualized returns of 6.0% by the end of 30 years.

EDIT: Using the above assumptions for a $500,000 portfolio with an initial 5% annual withdrawal (fixed at $25,000 per year, not taking into account taxes), here’s what two hypothetical retirement accounts would look like:

You’ll see that even with the exact same annualized returns, one account becomes completely depleted after 21 years, while the other one is still going strong.

How can that happen? It turns out that it’s not just the long-term average returns that impact your wealth, but the timing of those returns. Two people starting out with the same $500,000 portfolio at retirement can have entirely different outcomes, depending on when they start retirement. Someone starting out at the bottom of a bear market will have a much better chance of not outliving their retirement assets compared to someone starting out at a market peak, even if the long-term annualized rates of return are the same.

Our earlier post, Stock Market Returns Since The 2000 Peak And The 2009 Bottom is particularly relevant to this discussion, since there are multiple observations that suggest that market returns may be weaker going forward.

If you are nearing retirement or have recently entered retirement, it’s important to have a process to protect your wealth to mitigate the effects of Sequence Risk. Doing so can mean the difference between having a comfortable retirement or depleting your retirement account during your golden years.

Contact us today for a free consultation at (619) 888-4070 or email us at rainier@parabolic.us. We have a process in place to protect people at the most critical stage of their retirement, the five years before and the five years after retirement. See why one of the best investments you can make is to have an experienced and professional investment manager by your side.

(Posted October 10, 2014)

• Experienced: Over 15 years of experience, spanning three bull markets and two bear markets. Managed $100 million at Wells Fargo’s Wealth Management division and co-managed a $50 million hedge fund.

• Experienced: Over 15 years of experience, spanning three bull markets and two bear markets. Managed $100 million at Wells Fargo’s Wealth Management division and co-managed a $50 million hedge fund.

• No Conflicts Of Interest: You get unbiased advice because we don’t sell commissioned products. Fee is 1% of AUM (learn more).

• Your Interests Come First: We are held to the Fiduciary Standard, not the Suitability Standard.

• Avoid High Expenses: Index funds have up to 90% lower fees than actively-managed mutual funds and outperform them over the long term. Don’t own them? You may be paying too much.

Rainier Trinidad, CFA

San Diego and Coronado’s Fiduciary Financial Advisor

Parabolic Asset Management

206 J Avenue

Coronado, CA 92118

rainier@parabolic.us

(619) 888-4070

Investment Risk Disclaimers: (i) Investments involve risk and are not guaranteed to appreciate, and (ii) Past performance is no guarantee of future results.