This century’s Roaring 20’s is nothing like the one we had a hundred years ago. The only thing roaring this time around in 2022 was a bear, and it resulted in one of the worst years in history for the stock AND bond market. Stocks fell 18.1% for the 7th worst return in history:

And bonds fell 13.1%, which was the worst in history for the Aggregate Bond Index. Even supposed “inflation protected” bonds had a horrible year, falling 12.1%. Where’s the inflation protection when you needed it most?

And bonds fell 13.1%, which was the worst in history for the Aggregate Bond Index. Even supposed “inflation protected” bonds had a horrible year, falling 12.1%. Where’s the inflation protection when you needed it most?

To put the magnitude of these bond losses in perspective, in the 46 years since the Aggregate Bond Index started, there were only four down years before 2022, and its worst return was -2.9%:

1994: -2.9%

2013: -2.0%

2021: -1.5%

1999: -0.8%

At one point, government bonds (a subset of the aggregate bond index) had done so poorly that we had to go all the way back to the age of Alexander Hamilton to see returns this bad:

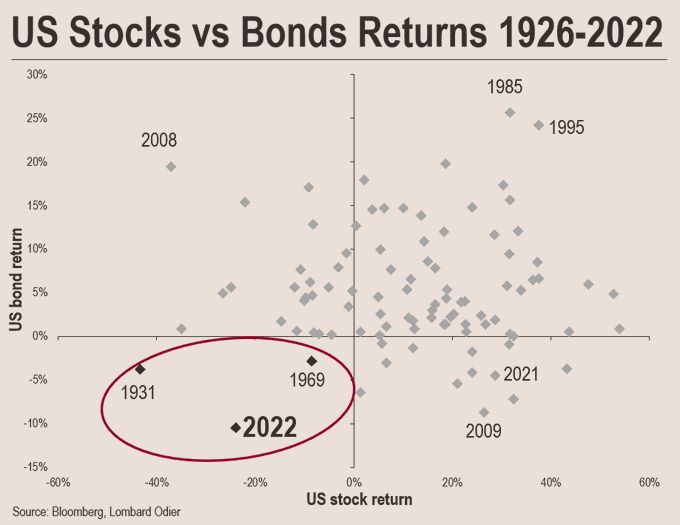

To see how rare it was for stocks and bonds to fall together for an entire calendar year, here’s a scatter plot that illustrates the three times in history it has happened:

Thankfully, we came into 2022 with some caution for stocks, which we wrote about here, and the ETFs we held with loss protections did a great job of shielding us from about half of the losses experienced by the stock market.

Thankfully, we came into 2022 with some caution for stocks, which we wrote about here, and the ETFs we held with loss protections did a great job of shielding us from about half of the losses experienced by the stock market.

But we weren’t as fortunate with bonds, at least initially, which for decades were considered safe investments and were used as anchors in a portfolio to offset losses if stocks fell. Even during the stagflationary era of the 1970s, stocks and bonds didn’t fall at the same time in any calendar year (see here).

The culprits in 2022 were many: Covid caused supply chain disruptions (people couldn’t work if sick, and the goods they couldn’t produce prevented other products down the supply chain from being manufactured, which caused prices to spike for the fewer goods that were available), the war in Ukraine caused energy prices to spike, and combined with ultra-low interest rates and lots of government stimulus initiatives from 2020, consumer demand coming out of the pandemic was massive, all of which caused prices to soar and the Federal Reserve to react by rapidly raising interest rates to combat inflation.

Our mistake for bonds was in believing the Federal Reserve when they tried to calm everyone down and said all of this was just “transitory” and that inflation would come down fairly quickly. Well they were wrong, and we were wrong to believe them (in hindsight it always seems so easy), and once it became clear they lost the inflation narrative in June, we adjusted our bond holdings quickly and became very defensive by moving to hold only the shortest duration (maturity) bonds and bond alternatives that weren’t as subject to the inflation narrative. By the end of the year, the Aggregate Bond Index fell another 3.5%, while the shortest duration bonds held up nicely and traded flat and the bond alternative ETFs we bought actually rose about 3.2%, so we were able to avoid some of the overall bond damage in 2022, around 25% from switching to short duration bonds and about 45% from switching to the bond alternative ETFs.

So did we do better than a passive strategy of holding the stock and bond indexes? Yes, by quite a nice margin, thankfully. But we know it’s never pleasant to see investment balances go down. The good thing is that since the losses were more moderate, it doesn’t take as much to recover. The same can’t be said for tech investors, which lost about 32% in 2022 (and more if you were unfortunate enough to own a higher concentration of mega cap tech stocks like Facebook, Amazon, or Tesla, which were down 50%-65%). A 10% loss needs an 11% gain to recover losses, while a 32% loss needs a 47% gain to get back to even.

Going forward, 2023 is going to provide some challenges and some possible opportunities, which we will write about in the next post.