According to the Labor Department (source), in 1979, 74 percent of workers participating in retirement plans had a defined benefit pension that would provide a fixed income stream. A defined benefit plan is one where the employer guarantees that your plan has a minimum value upon your retirement. This removes the worry that you’ll have an adequate enough investment return because it’s guaranteed by your employer.

Well, as time passed, many employers realized that investment returns weren’t keeping pace with actuarial projections – some had pegged the long term future growth rate at 10% – and it wasn’t turning out that way, thanks to events like the bear market of 2000-2002 and the 2008 Financial Crisis. The result? Employers ended up owing billions in pension payments and having unfunded liabilities on their balance sheets.

After making some uncomfortable adjustments, employers gradually came around to the thinking that they didn’t want the risk of providing a guaranteed investment return anymore (the defined benefit part), and instead decided to offload that risk to the employee by providing defined contribution plans, in which they’ll guarantee a certain deposit amount into your retirement account, but they no longer have to guarantee that it’ll be worth a certain value when you retire. That risk, unfortunately, is now on your shoulders.

By 2013, 93 percent of workers in retirement plans had defined contribution plans. It was now up to the employee to decide how they were going to invest the money, and they were left to fend for themselves and count on their own judgment to steer their investments.

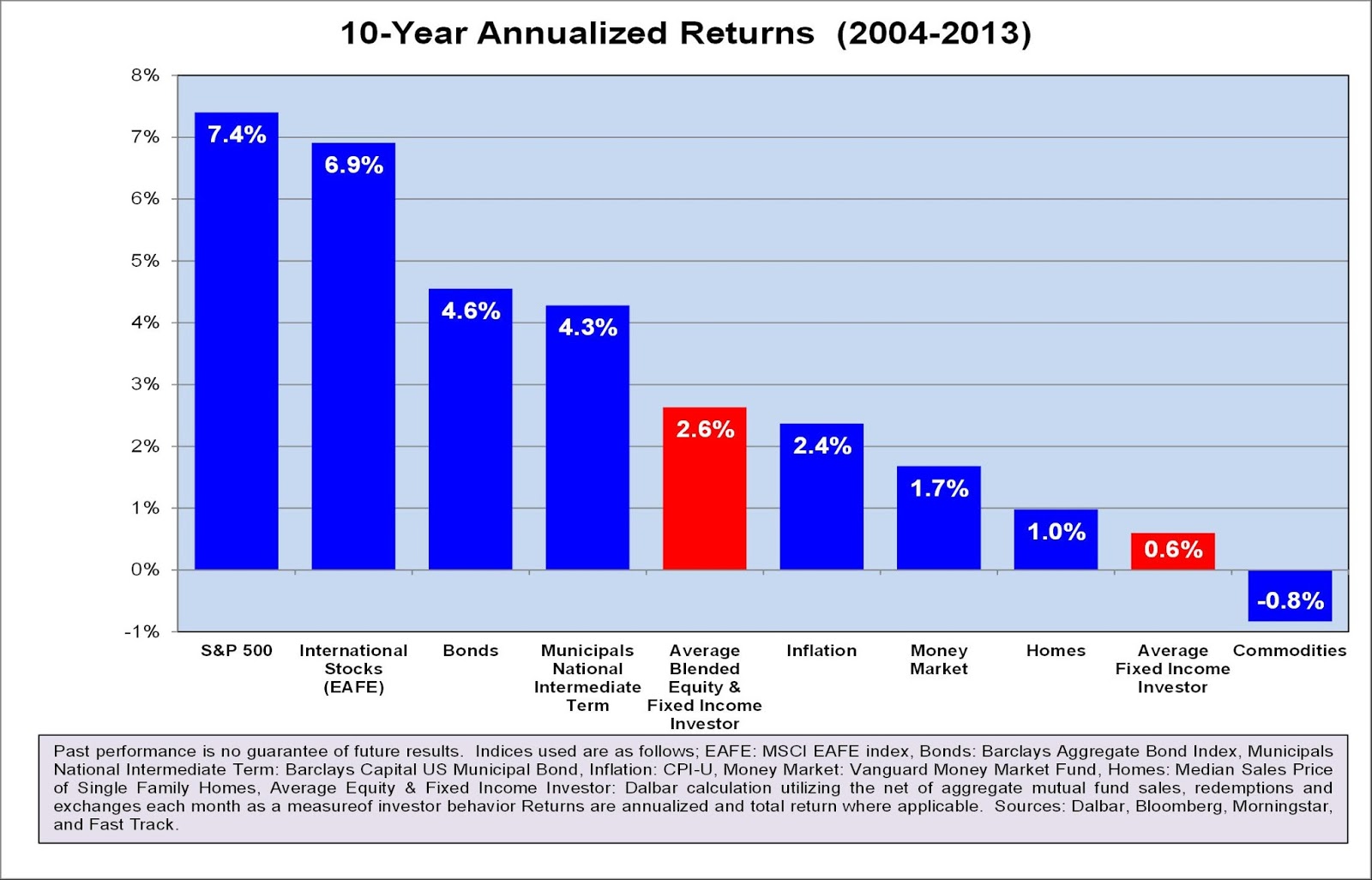

How did they do? Dalbar tracked the investment returns of individuals going back 10 years (2004-2013), and the results paint a troubling picture.

|

| (Click to enlarge) |

In an environment where the S&P 500 return 7.4% annually and bonds returned 4.6% annually, the average investor in a blend of equities and fixed-income mutual funds returned only 2.6% annually for the 10-year time period ending Dec. 31, 2013.

Investors generally have a very hard time separating their emotions from their investment decisions. Their tendency to buy when things are exciting and look safe and sell when markets are fearful and look dangerous are some of the biggest reasons for this underperformance.

If you’ve tried to manage your investments yourself and have increasingly felt that there might be a better way to invest, call us today and let us help get your retirement program back on track. There is a better way, and we can help. Vanguard has stated that having an investment advisor can add up to 3% in net returns per year by doing the following for their clients:

Being an effective behavioral coach. Helping clients maintain a long-term perspective and a disciplined approach is arguably one of the most important elements of financial advice. (Potential value add: up to 1.50%.)

Applying an asset location strategy. The allocation of assets between taxable and tax-advantaged accounts is one tool an advisor can employ that can add value each year. (Potential value add: from 0% to 0.75%.)

Employing cost-effective investments. This critical component of every advisor’s tool kit is based on simple math: Gross return less costs equals net return. (Potential value add: up to 0.45%.)

Maintaining the proper allocation through rebalancing. Over time, as its investments produce various returns, a portfolio will likely drift from its target allocation. An advisor can add value by ensuring the portfolio’s risk/return characteristics stay consistent with a client’s preferences. (Potential value add: up to 0.35%.)

All it takes is a simple phone call with our experienced portfolio manager who has been managing investments for over 15 years and has been helping investors reach their financial goals to help you get back on track. Contact us today for a free consultation at (619) 888-4070 or email us at rainier@parabolic.us.

(Posted July 6, 2015)

• Experienced: Over 15 years of experience, spanning three bull markets and two bear markets. Managed $100 million at Wells Fargo’s Wealth Management division and co-managed a $50 million hedge fund.

• Experienced: Over 15 years of experience, spanning three bull markets and two bear markets. Managed $100 million at Wells Fargo’s Wealth Management division and co-managed a $50 million hedge fund.

• No Conflicts Of Interest: You get unbiased advice because we don’t sell commissioned products. Fee is 1% of AUM (learn more).

• Your Interests Come First: We are held to the Fiduciary Standard, not the Suitability Standard.

• Avoid High Expenses: Index funds have up to 90% lower fees than actively-managed mutual funds and outperform them over the long term. Don’t own them? You may be paying too much.

• Held to the CFA Code of Ethics: Our firm believes in operating with integrity and abiding by the highest ethical and professional standards in the industry.

• Complimentary Portfolio Reviews: If you haven’t had your investment portfolio reviewed in over six months, it may be time for a checkup. Identify trouble spots and find ways to lower your fees at no charge. Give us a call at (619) 888-4070 or email us at rainier@parabolic.us. All portfolios are welcome.

Rainier Trinidad, CFA

San Diego and Coronado’s Fiduciary Financial Advisor

Parabolic Asset Management

206 J Avenue

Coronado, CA 92118

rainier@parabolic.us

(619) 888-4070

Investment Risk Disclaimers: (i) Investments involve risk and are not guaranteed to appreciate, and (ii) Past performance is no guarantee of future results.